Begin by unlearning the false assumptions of CAPM that led to these false conclusions:

- No one can beat the market on a risk adjusted basis.

- No one can time the market more often than not.

- No one can actively manage asset allocations.

- The best strategy is to buy and hold.

Our research refutes all of the above.

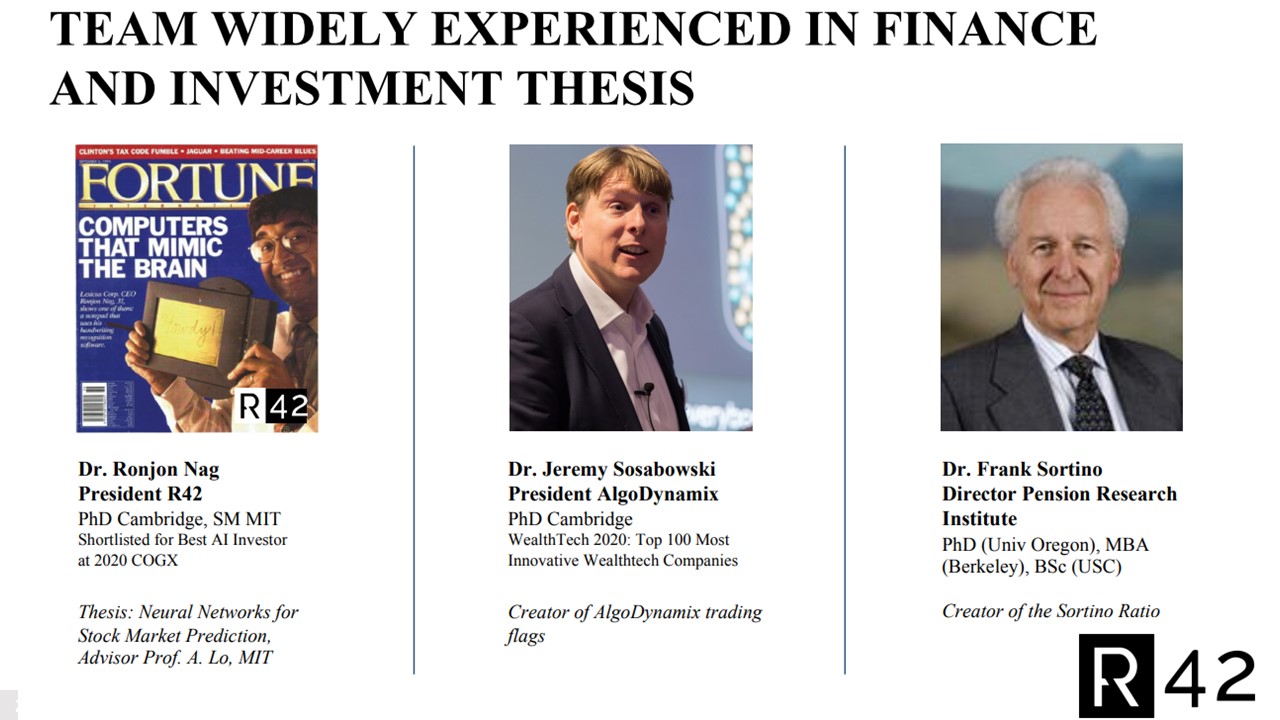

Who are we:

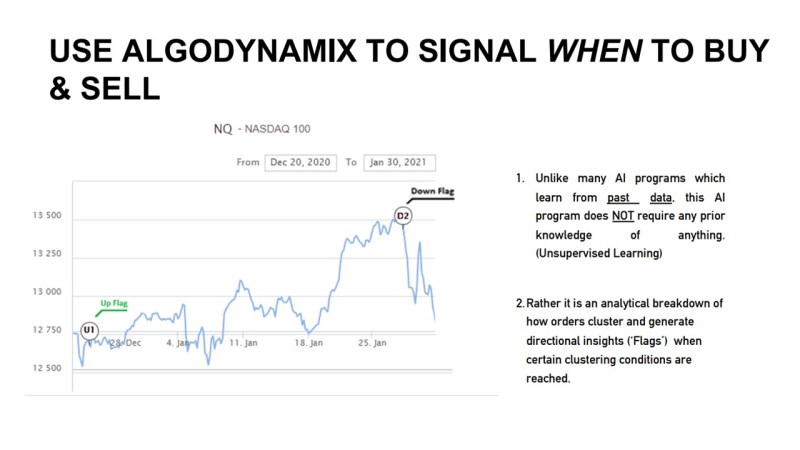

Methodology

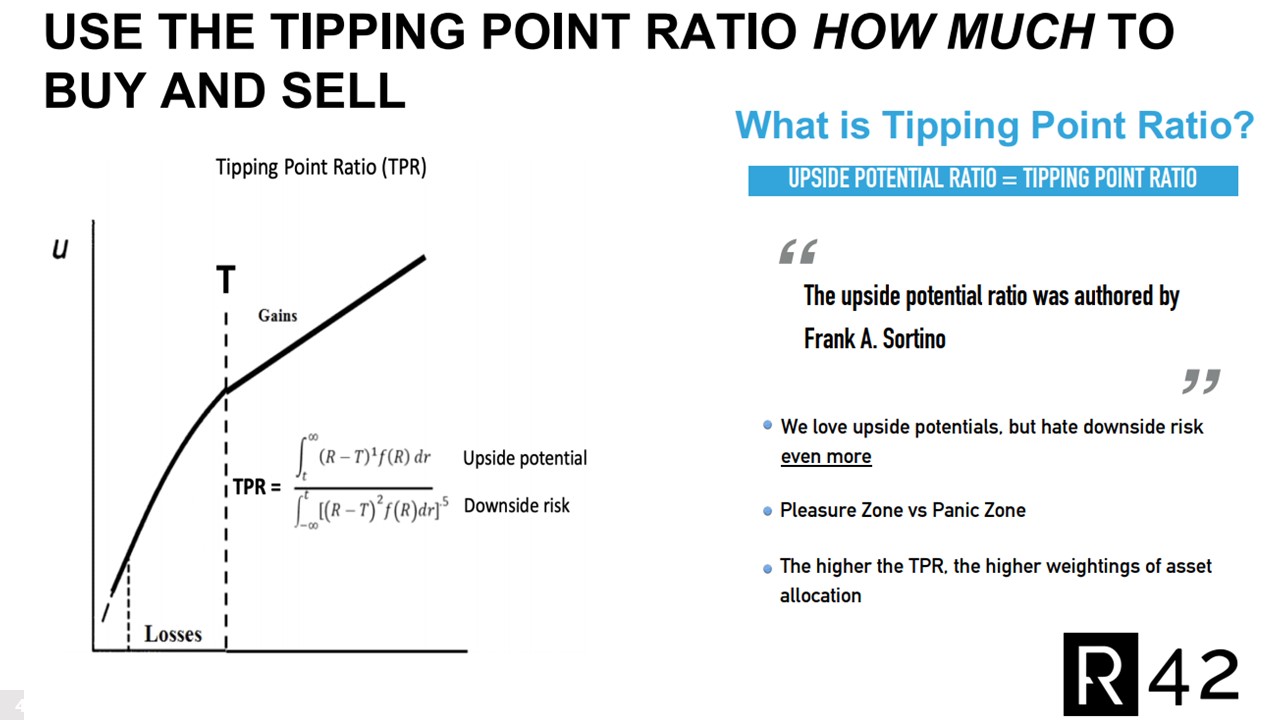

Forget about alpha and beta and focus on the Tipping point (T) that separates good outcomes from bad outcomes. Maximize the Upside Potential above T relative to the downside risk below T and forget the Sortino and Sharpe ratios. TPR is the New Sortino Ratio.

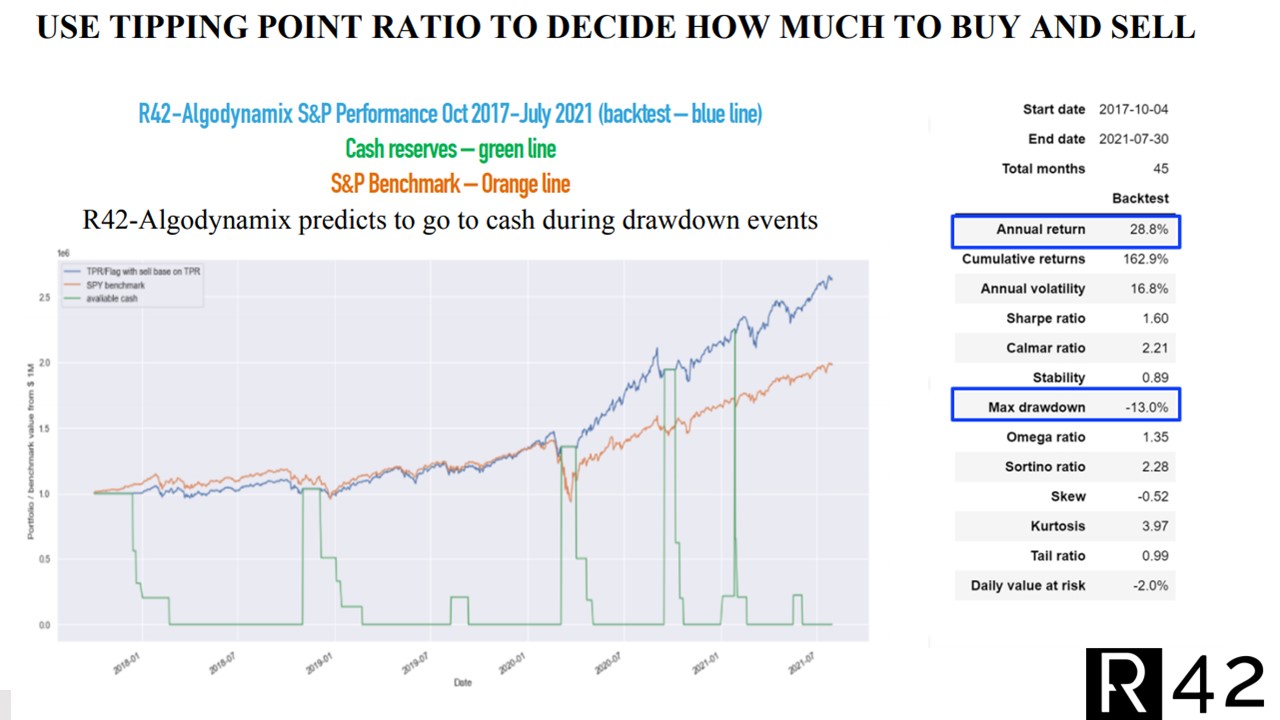

Results

Of course, past results from back tests do not guarantee future results anymore than Big Blue’s results guaranteed it would beat the world chess champion, or that Google’s AI model would beat Big Blue, or that another Google AI model would beat the world’s GO champion.

For more details contact The R42 Institute, Palo Alto, California