Frank Sortino & Kal Salama

In an Uncertain World

If you believe the uncertainty associated with investing in the indexes shown in Figure 1 is bell shaped, and it is not, all your metrics for performance measurement and asset allocation will be wrong. Well, the law of large numbers may be right in the long run, but we all live and operate in the often skewed world of the here and now. This paper offers a tool for recognizing those times when there is more downside risk than upside potential and vise versa and how to manage it better by formally recognizing a different shape to uncertainty that is better suited to the task at hand.

That “better shape” is the brain child of two professors at Cambridge University, Aitchinson and Brown, who developed a form of the lognormal distribution that can use negative as well as positive returns to skew the distribution either left or right. Fortunately, you don’t need a PhD in mathematics to calculate the shapes shown in Figure 1. All you need is the Forsey-Sortino model; a simplified version of software that Professor Emeritus in Mathematics, Hal Forsey and Professor Emeritus in Finance Frank Sortino developed at the Pension Research Institute (PRI) at San Francisco State University. And all you need to know as inputs to the model is what you already know: the average return and standard deviation of each index, plus one more return that we call: the Desired Target Return®, or DTR®. Given the better shape, the model can then calculate better statistics. Better, in that one could have beat the market more often than not over the past 26 years. Of course, the more people who use this model, the less inefficiencies one would expect to find in the stock market. History indicates that will not be a problem.

Figure 1

The picture on the left is the positively skewed large core equity index (LC) and the picture on the right is the negatively skewed small cap growth index (SG). If you are forced to viewing both of these indexes as symmetric, bell shaped distributions, you may well conclude that you should just buy the market index because in the long term, the market is bell shaped, and everyone knows, you can’t beat the market, right? Maybe not. The key forecasting element in Figure 1 is the Upside Potential ratio (UP ratio)[1], which was first mentioned in an article published with my Dutch friends’ way back in 1991. PRI has repeatedly recommended replacing the Sortino ratio with the UP ratio, but to no avail. We will conduct three tests to indicate the superiority of the UP ratio.

The picture on the left is the positively skewed large core equity index (LC) and the picture on the right is the negatively skewed small cap growth index (SG). If you are forced to viewing both of these indexes as symmetric, bell shaped distributions, you may well conclude that you should just buy the market index because in the long term, the market is bell shaped, and everyone knows, you can’t beat the market, right? Maybe not. The key forecasting element in Figure 1 is the Upside Potential ratio (UP ratio)[1], which was first mentioned in an article published with my Dutch friends’ way back in 1991. PRI has repeatedly recommended replacing the Sortino ratio with the UP ratio, but to no avail. We will conduct three tests to indicate the superiority of the UP ratio.

How it works:

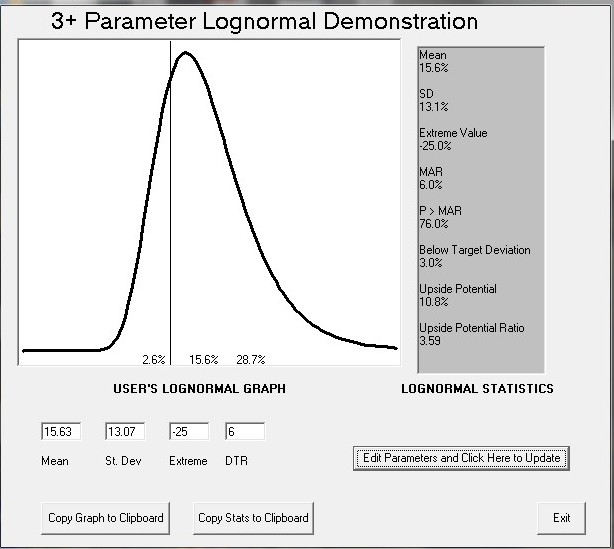

Imagine two investment committees with two different investment objectives. The first investment committee is a foundation that needs to earn 6% annually to meet their scheduled philanthropic payouts. The second investment committee has a defined benefit plan and their Desired Target Return (DTR®) is the actuarial rate of return of 8.5%. Both committees use the Forsey-Sortino model (F-S model) shown in Figure 1 that can calculate the UP ratio on data provided by their consultant. Beginning in 1990 they both use the average return and standard deviation for the last three years as input to the F-S model. Figure 2 shows how the foundation would key in the historic data and DTR of 6%.

Figure 2

The output from the F-S model is shown in the right hand side of Figure 2. The UP ratio of 3.59 means this large value index they own has 3.59 times more upside potential than downside risk. The committee intuitively understands that upside potential is good and downside risk is bad.[2] They don’t know how these terms are calculated, nor do they care. They decide to see if some combination of the nine style indexes they own could beat the market the following year by using the UP ratio. The pension committee acted the same as the foundation, only they used the actuarial return of 8.5% as their DTR. Based on this simple framework, both committees performed three tests:

First Test: Can an Asset Allocation based on the UP ratio perform better than the market mix of 60% S&P 500 and 40% Barclays A+ Aggregate bond index? Any negative UP ratios will be allocated to the bond index.

Second test: Holding the 60/40 asset allocation constant, can the UP ratio weights select style indexes that beat the 60/40 market mix?

Third test: Can the UP ratio select equity style Indexes, remaining 100% in equities, that beat the S&P 500?

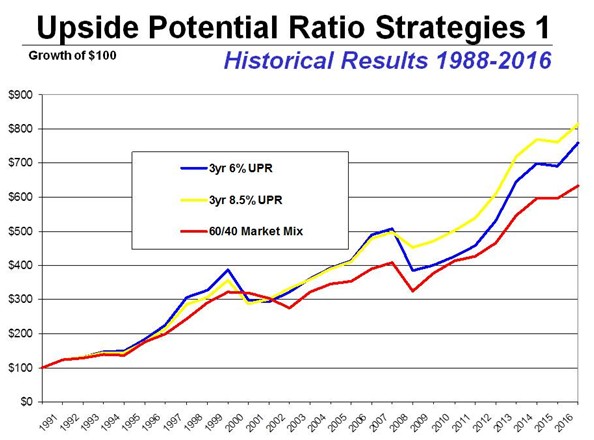

Figure 3 presents the results they would have seen on the first test year after year.

Figure 3

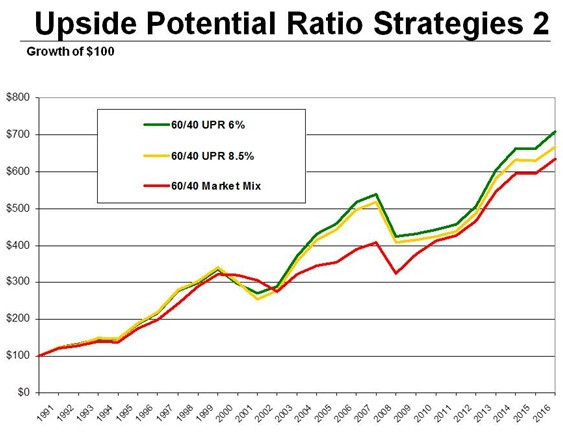

In 15 of the 26 years the UP ratio 6% strategy (UPR) beat the market mix. In one year it beat the market mix by less than 100 basis points so they called that a tie. The market mix beat the UPR 6% strategy 10 times; so, using the UP ratio won 50% more often than the 60/40 market mix. That is astounding. The pension committee, using a DTR of 8.5%, found the UP strategy beat the market mix as often as it lost but earned a higher cumulative return. Importantly, this shows the sensitivity of the UP ratio to the return the user needs to earn in order to accomplish their investment objective. When the committees held the asset allocation mix constant to test the ability of the UP ratio to add value, by identifying sectors of the market that would perform better than the S&P 500, they got the second test results shown in Figure 4.

Figure 4

Once again both UP ratio strategies beat the market mix even when the asset allocations were held to a 60/40 mix. So, it wasn’t just the asset allocation decision that was adding value. It was something buried in the calculus used to generate the picture of uncertainty shown in the F-S model output.

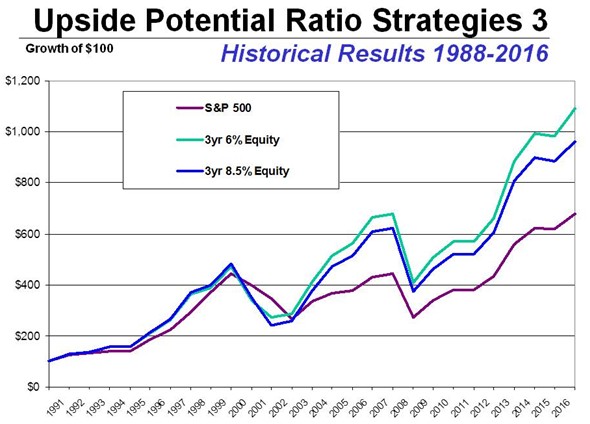

Third test: Can the UP ratio weighted equity style Indexes beat the S&P 500?

The all equity 6% UP ratio strategy averaged 9.63% versus 7.64% for the S&P 500 over 26 years. The all equity 8.5% UP ratio averaged 9.10% over 26 years.

The S&P 500 was only able to beat the UP ratio strategies 6 out of the 26 years and two of those times it was by less than 100 basis pts.

Figure 5

Figure 5 shows using the UP ratio weights to invest in the indexes while remaining 100% in equity performed better than the S&P 500 most of the time over the past 26 years, in spite of the fact that the three year interval following the 2008 market collapse resulted in negative UP ratios for all indexes. To ensure we were measuring 100% equity in both strategies, we assumed all funds were invested in the S&P 500 for these three years.

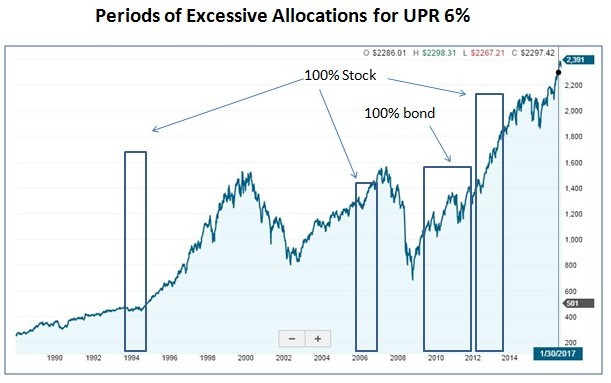

Figure 6

The tests above were performed with no constraints on the asset allocations. The result shown in Figure 6 identifies years when excessive allocations (100% Stock or 100% Bond) were made that could be considered outside of acceptable investment policy guidelines due to lack of diversification. The F-S model was developed as a tool to be used by financial professionals to make better portfolio decisions. The authors caution that the model should not be the decision maker.

We now return to Figure 1, repeated below, for a more detailed explanation of the otherwise unavailable information disclosed in the F-S model output.

Figure 1

On the left is the forecast for the Surz large centrix index (LC) which had the highest UP ratio of the nine Surz Style Pure indexes®. LC is all the stocks that are neither growth nor value. This is different than all other core style indexes which are a mish-mosh of everything (For more details see www.ppca-inc.com.). The UP ratio of 1.66 indicates It has 66% more upside potential than downside risk. Because the mean is positive it is anchored at -25% causing the shape of uncertainty to be positively skewed, not symmetric and not a normal or bell shape.

The small cap growth index shown on the right has a negative mean of -3.01% so we anchored it at +25% causing it to be negatively skewed with below target risk of 23.3% as opposed to 4% for the LC index. This obviously had the worst UP ratio. While there is a 41% chance returns could be above 6%, the UP ratio of .12 indicates this index has 88% more downside risk than upside potential. If one doesn’t believe the inputs, you can play,” what if” games by changing them. This is unique information one should want to know. We don’t believe any other model has this information with only these 3 inputs. How did these projections do so far? As of June 1st the LC index was up 8.4% and SG was up 2%.

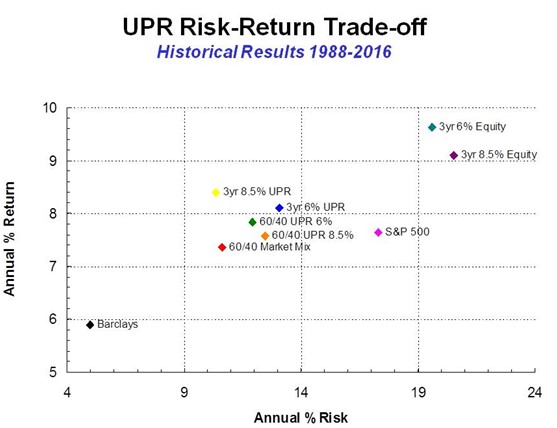

The Traditional Picture

Figure 7

Traditional mean-standard deviation risk measures would make the all equity UP ratio strategies appear to be the most risky over the last 26 years; highest return and highest risk. Nobody would choose the S&P 500 risk-return trade-off and everybody would choose the 8.5% UPR, really? If someone measured risk relative to their DTR and most of the volatility was above the DTR? Risk for the committee members in this study is not a bumpy ride, it is that they don’t accomplish their investment objective, causing a failure to accomplish their goal of a specified pay out. For them, beating the market is not the goal and is not the investment objective. For them, the traditional framework of performance measurement is misleading. For them, performance should be measured relative to their DTR, as shown in the Journal of Performance Measurement, Summer 2016.

Summary & Conclusions:

To prove to yourself that the Forsey-Sortino model offers you valuable information not available anywhere else, download the model as shown below and follow these steps:

- Enter the means and standard deviations shown at the bottom of Figure 1. Then see if the upside potential ratios give you indications of which styles to emphasize and which to deemphasize. Does this provide a unique insight?

- Enter the year end means and standard deviations of the three best performing and worst performing assets in your portfolio and see if the information in the F-S model would have been useful, given current results.

Please direct all responses to:

Kal Salama, CFA

Chief Investment Officer

The Headlands Group, Inc.

(415)464-9144

kal@headlandsgroup.com

http://www.headlandsgroup.com/

https://www.linkedin.com/in/kalsalama

https://www.linkedin.com/in/kalsalama

To download the software: Control click on the highlighted link below, install the VBruntime.exe file to ensure your computer can run software written in Visual Basic. Then install and run the F-S model.

The Forsey-Sortino Model-1 software

This dropbox link may ask you to sign in but at the bottom you can skip this step. This zip file contains two files: Forsey-Sortino.exe and a Microsoft VBRuntime.exe. If you get an error message with F-S Sortino.exe you must install the enclosed VB runtime.exe.

[1] Sortino, F., van der Meer, R.A.H and Plantinga, A (1999) The Dutch Triangle, Journal of Portfolio Management, Fall

[2] Researchers at Groningen University in The Netherlands found that people they interviewed intuitively understood these terms without having to explain exactly what upside potential or downside risk were or how they were calculated.

Pingback: More Downside Risk than Upside Potential? | Salt Creek Investors

Thank you for using my software. I’m sorry we never had a chance to talk about it. Best of luck

Frank